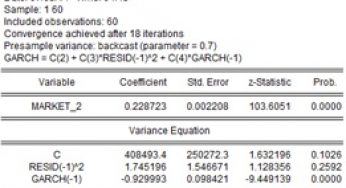

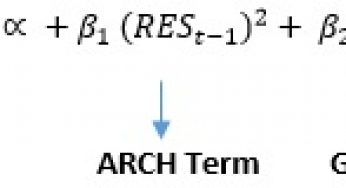

Volatility models by ARCH & GARCH econometrics using eviews In order to investigate Volatility models by ARCH &… Read More

Concept of volatility If the water changes to gas then this is called volatility. Similarly, if data has… Read More

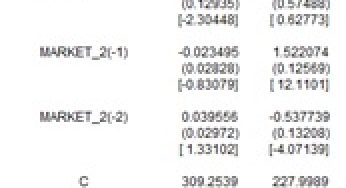

Autoregressive distributed lag model The above model contains ARDL (autoregressive distributed lag model) in addition to VAR / vector… Read More

The prediction of dependent variable by the predictors (independent Variable) is called regression. If the previous lags of… Read More